Understanding the difference between a home inspection vs. home appraisal can be tricky. Both occur during the homebuying process and assess the for-sale property. Both are also crucial, if not required, for a smooth home sale.

In actuality, though, they’re quite different. Each accomplishes a different purpose and requires a different process.

If you’re buying or selling a home, you’ll probably come across these terms. You may even see them listed as part of your closing costs. So, understanding them is necessary.

Below, we discuss home inspections and home appraisals in full. We’ll cover what they are, how each process works, and why you need them. We’ll also talk about when to use each, even outside the homebuying process.

So if you want to learn the difference between home inspections vs. home appraisals before buying a home for sale in Boynton Beach, FL or anywhere in the US, read on.

What Is a Home Inspection?

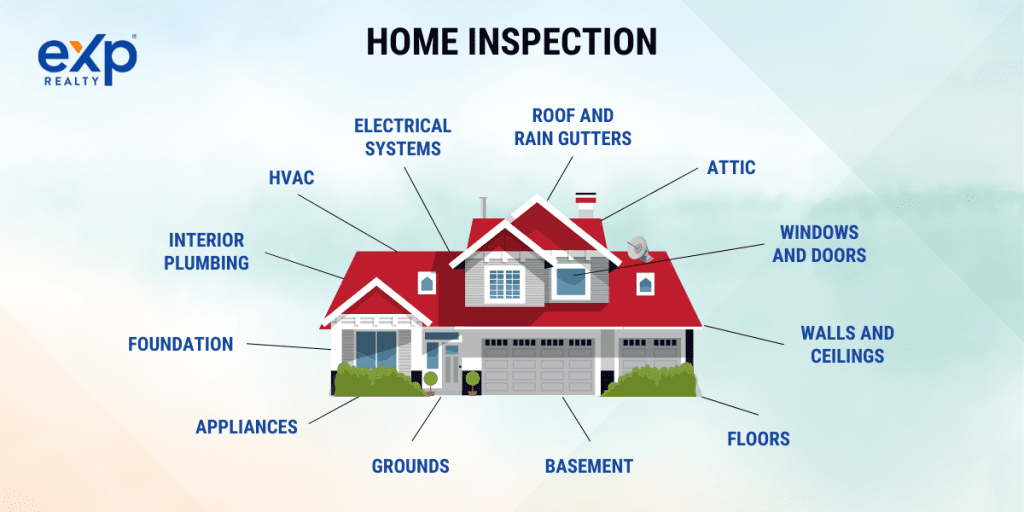

A home inspection is a comprehensive evaluation of a property’s condition. It focuses on structures and major systems, with the ultimate aim of discovering any current or potential underlying issues.

During a home inspection, a licensed inspector will examine several aspects of the home, including the:

- Roof

- Attic

- Basement

- Electrics

- Plumbing

- HVAC

They’ll also look for any water damage or other structural issues, like plaster cracks in pools, that could suggest problems later on. Then, they’ll record their findings in an inspection report.

The Home Inspection Process

The potential home buyer usually requests a home inspection. When they submit an offer on the property, they’ll typically include an inspection contingency. The contingency means the offer depends on the home inspection result.

Typically, the buyer pays for the home inspection. The average cost is between $300 and $400, which buyers will see listed with their closing costs.

Professional home inspectors usually encourage buyers to be there during the inspection. This allows the inspector to point out issues or potential issues in person, ensuring the buyer understands the property’s current condition.

If the buyer can’t be there, they may send their real estate agent in their stead.

The seller, however, should not be present at the inspection. Having the seller there can create unnecessary tension between the buyer and seller during a volatile time. Sellers may be insulted by buyer comments regarding the home condition, and buyers may feel uncomfortable asking detailed questions in front of the current homeowner.

The inspector will use an inspection checklist to help ensure an accurate home inspection.

Starting with the grounds, they’ll look for evidence of poor drainage or septic leaks. They’ll also look for any trees that could be a safety issue later.

The inspector will go on to check the home’s exterior. And, though they won’t physically climb onto the roof, they’ll do a visual inspection, checking for broken or missing shingles and signs of decay.

They’ll also check for foundation cracks, missing weather stripping on windows, and cracks near door frames.

Inside, the inspector will check for things like signs of moisture in basement areas. They’ll ensure that the electric panel has the proper connections and that the water heater is the right size for the home. They’ll also inspect any crawl spaces for signs of damage and make sure the home’s ventilation is adequate.

The inspector will go on to check each room for safety features, like smoke alarms and carbon monoxide detectors. They’ll check bathroom and kitchen plumbing and ensure the HVAC system works.

If the home inspector discovers major issues, the buyer has a few options. They can negotiate with the seller to cover all or part of the repairs. Or, they can choose to withdraw their offer.

Additional Home Inspections

While the inspection process will catch most major issues, it won’t catch everything. Sometimes home buyers might want to request additional, specialized inspections for things like:

- Radon gas

- Termites and other pests

- Mold

Inspections for mold, termites, and radon gas require special equipment and training. Most licensed home inspectors don’t have the knowledge or tools to find them.

The Importance of Home Inspections

In most cases, neither general home nor specialty inspections are required. And, in competitive markets, buyers sometimes offer to waive the inspection. However, buyers may want to think twice before doing so.

A home inspection is incredibly valuable. It reduces buying risks, reveals needed minor repairs, and can help buyers feel safe in their new home. They won’t have to worry about the home’s structural integrity or fear future costly repairs.

And, if major issues need to be addressed, buyers can negotiate with the sellers. Those negotiations could lead the seller to reduce the sales price.

What Is a Home Appraisal?

A home appraisal is a professional evaluation of the property’s worth. It estimates the home’s fair market value and lets lenders know whether the property’s worth is enough to justify the mortgage loan amount.

In a home appraisal, the professional appraiser will look at several factors to determine a home’s value. These include:

- Location

- Property condition

- Home age

- Home design

- Square footage

- Home improvements

Appraisers will also research the value of recently sold homes in the area and consider any blatant signs of disrepair, like obvious water damage or a decaying roof.

The Appraisal Process

During the buying process, after the seller accepts the buyer’s offer, the loan provider may hire a licensed appraiser to assess the home’s market value.

Almost every mortgage loan requires a property appraisal. Cash buyers and those receiving less than $400,000 in private financing may skip it.

However, VA and FHA loans require a home appraisal regardless of the amount. Given all of these factors, the vast majority of estate transactions will include an appraisal.

The mortgage loan company will choose the appraiser, but the buyer usually pays for it with their closing costs.

During the appraisal, a licensed professional will use an appraisal checklist to do in-depth research on the home and surrounding area. They’ll gather background information online by looking at current listings, researching local construction costs, and examining municipal records regarding the property.

They’ll pay special attention to “comps” or comparables. A comparable is a recently sold or listed property similar to the appraisal property. It will have similar amenities, be of equal quality, and be close to the same age.

If the mortgage company requires a walk-thru appraisal, they will contact the seller or seller’s agent to arrange a date and time. During the walk-thru, they’ll visually inspect the interior and exterior of the property.

In some circumstances, the appraiser may not need to walk through the home. Instead, they can do a drive-by appraisal, allowing them to develop a decent picture of the home’s exterior and surrounding community.

Once their research is complete, the appraiser will assemble an appraisal report. They give a copy of this report to the borrower and the lender. In it, they’ll list an estimate of the home’s fair market value.

The loan provider cannot lend for more than 97% of the appraised value. If the appraisal is too low, the buyer can either:

- Pay the difference in cash

- Renegotiate the sales price

- Walk away from the sale

The Importance of Home Appraisals

Most real estate transactions include a home appraisal. Though it may seem like it only helps the buyer’s loan provider, in reality, it provides utility to the buyer as well. An appraisal ensures the buyer isn’t overpaying for a property. It also ensures they pay the correct property tax.

If the house appraises for significantly less than the selling price, it may give the buyer leverage to negotiate a price reduction.

Of course, in a competitive market, it’s crucial to note that the seller may push forward with a list price well above the latest appraisal in hopes of a cash buyer. That’s why it’s often a good idea for cash buyers to use appraisals as well. Even though they’re not securing financing, a cash buyer can use an appraisal to ensure they’re paying a fair price.

Key Differences Between Home Inspection and Home Appraisal

When looking at home inspections vs. home appraisals, it’s easy to see their similarities. Both take place during the homebuying process, and both assess the property for sale. However, there are some key differences.

Purpose

The biggest difference between an inspection and an appraisal is the purpose behind them. A home inspection identifies current and potential problems with the property. A home appraisal determines a property’s value.

Content

Home inspections and appraisals are both assessments. However, they consist of very different things.

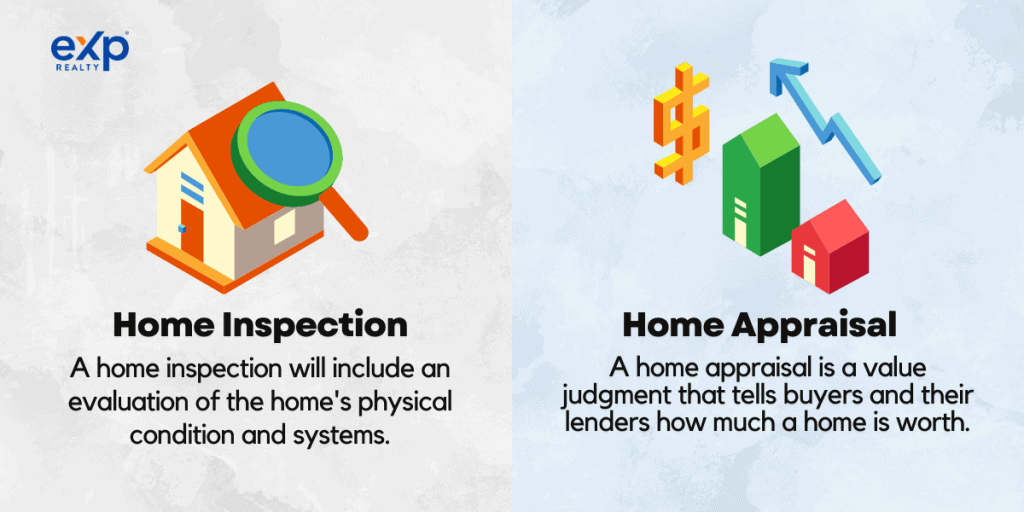

A home inspection will include an evaluation of the home’s physical condition and systems. It gives an in-depth picture of the home’s inner workings and offers buyers a decent understanding of repairs that might be necessary.

A home appraisal is a value judgment that tells buyers and their lenders how much a home is worth. They base this on market conditions and comparable properties. In some cases, the appraiser doesn’t even need to step foot in the home.

Person Responsible

The buyer pays for both the appraisal and inspection in their closing costs. However, the person responsible for each is different. A licensed home inspector will complete the inspections. This person has typically taken classes on home inspection and applied through the state for a license.

A licensed and certified appraiser handles the home appraisal. They must meet the requirements set by their state and the Appraiser Qualifications Board (AQB). These requirements include education standards, experience hours, and a licensing exam.

When to Use a Home Inspection vs. a Home Appraisal

When buying a home, you’ll likely pay for both a home inspection and a home appraisal. However, those aren’t the only times you may need one or the other.

When to Use a Home Inspection

- When you’re selling a home. Hiring an inspector to identify any issues that may hinder a home sale later on may be a good idea. This is especially true if you’re selling a home you haven’t lived in. An inspection can help you set a fair price or identify repairs before putting the house on the market.

- As part of home maintenance. A home inspection can help point out issues or potential issues, allowing you to make repairs before you have a dangerous or more expensive problem.

- When you suspect an issue. If you’re worried about pest damage, suspect mold, or think there might be a crack in your home’s foundation, a home inspection can help give you peace of mind.

When to Use a Home Appraisal

- When you’re selling a home. A home appraisal can help you set the right price, allowing you to sell your home faster.

- When you’re refinancing. When refinancing a mortgage, the refinancing company will ask for a home appraisal.

- When you’re filing for divorce or bankruptcy. You’ll probably need a home appraisal as part of the court proceedings.

- For tax assessment purposes. Sometimes, you’ll need a home appraisal to determine the correct property taxes. For example, if you’re appealing the assessed value of your home, you may need a home appraisal.

Key Takeaways

Learning the difference between home inspections vs. home appraisals is crucial if you’re buying or selling a home. Both assess the for-sale property, but for different reasons. Home inspections evaluate the home’s condition, while home appraisals evaluate the home’s market value.

A good real estate agent will help you navigate the home inspection and appraisal process. So, if you’re interested in buying or selling, contact a local eXp agent to help. And if you’re interested in properties for sale near you, use our property search tool. You can even sign up to receive alerts when new listings come on the market.

FAQs

Understanding home appraisals vs. inspections tends to bring up questions. Let’s see if we can answer a few of the most common ones.

Do inspection and appraisal happen at the same time?

No, inspections and appraisals both occur during the home buying process, but not concurrently. The home inspector and appraiser will schedule different inspection days and times.

What is the difference between an inspector and an appraiser?

An inspector evaluates the home’s condition. They’re knowledgeable about structural issues, as well as home systems like electrics and plumbing. An appraiser assesses the home’s market value. They’re market experts who can estimate how much a home is worth given current conditions.

What fails a home appraisal?

A home appraisal that comes in lower than the seller expects can be due to a few common problems. These include square footage miscalculations or the failure to account for recent renovations. If the seller believes the appraisal was inaccurate, they can ask the buyer for a second one. In some cases, the lender will require another appraisal.

Assuming the calculations are accurate, the lender won’t be able to finance the full amount of the home. By law, they can only finance 97% of the home’s appraised value. This means the buyer can either pay the difference in cash, renegotiate the price with the seller, or walk away from the transaction.

What is checked during an appraisal?

During an appraisal, the appraiser checks factors that affect the value of the home. This includes the home’s condition, recent renovations, and comparable properties that recently sold or are for sale.

What happens if an appraisal comes in lower than the offer?

If the appraisal comes in lower than the offer, the mortgage lender will be unable to provide the full loan amount. At that point, the buyer can pay the difference in cash, renegotiate the home’s sale price with the seller, or walk away from the sale.

How much does an appraisal cost?

Appraisal costs vary by state, but generally, you can expect to spend between $400 and $600. This expense is usually added to the buyer’s closing costs.

How much is a home inspection?

Home inspection costs vary by location, but most range from $300 to $500. The home inspection fee is usually listed under the buyer’s closing costs.

What hurts a home appraisal the most?

The biggest factors that affect a home’s appraised value are its age and condition. The current market will also play a major role. An older home with outdated systems, like an old water heater or out-of-date HVAC system, will have a lower market value. If the local area is experiencing a drop in home prices, this will also hurt the appraisal value of the home.

Does a messy house affect an appraisal?

A messy house will not affect an appraisal. However, signs of neglect may influence the appraiser’s estimated home value. Chipping exterior paint, decaying outbuildings, or damaged flooring may lower the market value of the home.

What do home inspectors look for?

Home inspectors are looking for signs of damage and decay. They’re also looking for issues or potential issues with home systems, like plumbing or HVAC. Excess moisture, signs of leaks, structural cracks, and issues with electricity are all examples of what may come up in an inspection report.