Buying a home is usually the most important financial journey you’ll make in your life. During the course of the home-buying process, you’ll find yourself learning more about real estate, debt, and property law than you ever thought possible. Following a guide to creating a homebuying budget is key to being successful in the home-buying process, whether you’re operating in Chicago real estate or Chattanooga.

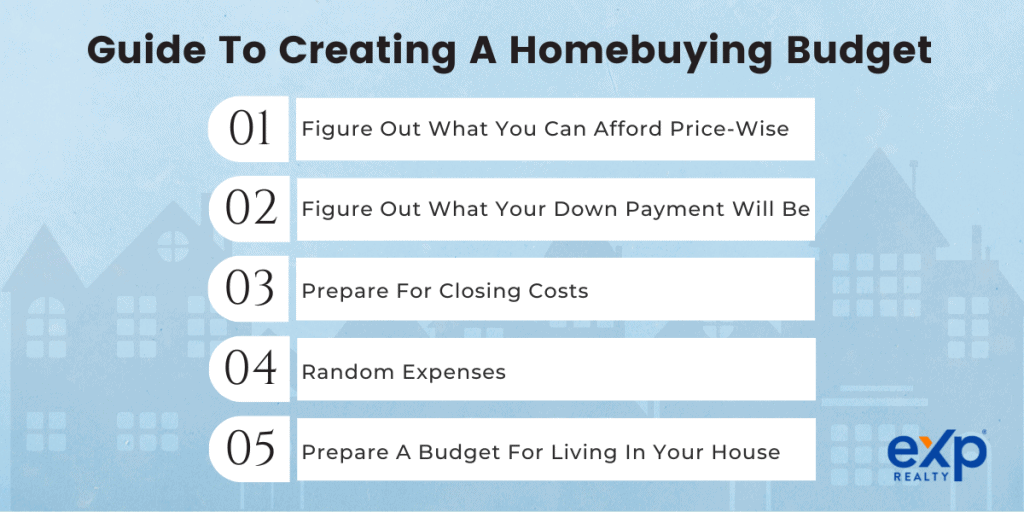

What To Base Your Budget On

The main expenses related to purchasing a home all revolve around two things: the purchase price of the home and the size of the loan you’ll need to take out to buy said home. If you don’t plan on taking out a loan and instead are going to pay the full price in cash, your guide to creating a homebuying budget may look a bit different.

Step One: Figure Out What You Can Afford Price-Wise

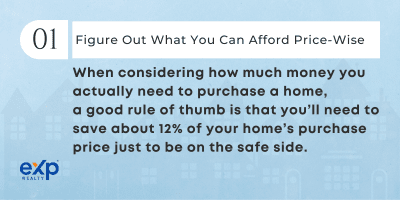

The homebuying budget begins with a purchase price. Of course, you won’t know the purchase price of the home you want until you’ve found the home you want. But you should be creating a homebuying budget well ahead of time. So first consider what price range you can afford. When considering how much money do you actually need to purchase a home, a good rule of thumb is that you’ll need to save about 12% of your home’s purchase price just to be on the safe side.

With a current median home price of $440K, that comes out to about $52K. Of course, bear in mind that your first home will probably not be your only home, and that starter homes in the US regularly list for between $150K and $250K. So even at the high end of the starter-price range, you’re looking at about $30K. Our estimate is a conservative estimate as well, which we’ll break down shortly. Our main aim is to save you money in the long run by urging you to prepare for the worst and hope for the best.

With a current median home price of $440K, that comes out to about $52K. Of course, bear in mind that your first home will probably not be your only home, and that starter homes in the US regularly list for between $150K and $250K. So even at the high end of the starter-price range, you’re looking at about $30K. Our estimate is a conservative estimate as well, which we’ll break down shortly. Our main aim is to save you money in the long run by urging you to prepare for the worst and hope for the best.

Step Two: Figure Out What Your Down Payment Will Be

Let’s quickly do away with the myth that you must put down at least 20% of your home’s value when purchasing a house. Though this is a good way to avoid paying Private Mortgage Insurance, a monthly premium tacked onto your monthly mortgage payments, if it wipes out your savings it’s doing you much more harm than good.

Americans put down 6% on average when buying a home, while many first-time homebuyers don’t put down anything at all. In most cases, 0% down payments are facilitated by government-backed loans such as USDA loans and VA loans, and loans with down payment requirements as low as 3.5% with FHA loans (FHA loans aren’t actually loans, instead the Fair Housing Administration will insure whatever loan you take out with a conventional lender). Even if you don’t qualify for any assistance programs, first-time home buyers with good credit can still make down payments as low as 3% with Conventional 97 and HomeReady Loans.

As you can see, your down payment does not have to be an overwhelming expense of the home-buying process. If you’re a first-time homebuyer without the savings that established property owners benefit from selling a previous home, it makes sense to get the lowest downpayment you can.

The good thing about making a large down payment on a home is that it diminishes the size of the loan you must take out to cover the rest. The lower the loan, the less you’ll pay on the closing costs that are calculated on your debt, and not your home’s value.

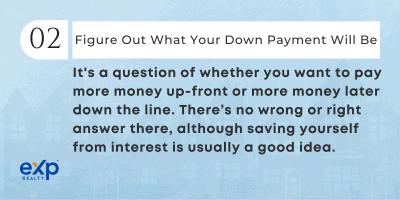

It’s a question of whether you want to pay more money up-front or more money later down the line. There’s no wrong or right answer there, although saving yourself from interest is usually a good idea. Talk to your real estate agent about what other homebuyers in similar circumstances as yours have done in the past, and you’ll have a clearer understanding moving forward.

It’s a question of whether you want to pay more money up-front or more money later down the line. There’s no wrong or right answer there, although saving yourself from interest is usually a good idea. Talk to your real estate agent about what other homebuyers in similar circumstances as yours have done in the past, and you’ll have a clearer understanding moving forward.

But while you’re just getting started creating a homebuying budget, bet on a 6% downpayment, and you’ll either be right on the mark or even save yourself money in the long run.

Step Three: Prepare For Closing Costs

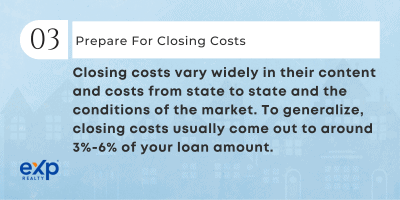

The dreaded big C’s of homebuying are among the hardest things to pin down when it comes to creating a homebuying budget. Closing costs vary widely in their content and costs from state to state, regions within the state, and the conditions of the market. Law and tradition come together to determine who pays what, the buyer or the seller, and whether or not a lawyer must be present at closing. To generalize, closing costs usually come out to around 3%-6% of your loan amount.

In states with high closing costs like Pennsylvania, Maryland, and Connecticut, these high costs come less from the expenses themselves and more from taxation. Taxes set aside, most of the time closing costs amount to between $2K and $4K. To be on the safe side, assume you’ll be paying $4K with an extra $1K for taxes.

In states with high closing costs like Pennsylvania, Maryland, and Connecticut, these high costs come less from the expenses themselves and more from taxation. Taxes set aside, most of the time closing costs amount to between $2K and $4K. To be on the safe side, assume you’ll be paying $4K with an extra $1K for taxes.

Step Four: Random Expenses

Random expenses could be anything from moving costs to renting storage space for when you’re showing your home to potential buyers. Most likely these costs won’t set you back too far. Renting a U-Haul is usually about $50 a day with fees added on. Hiring out the labor of a moving company is much more expensive but easier on your back, though not on your wallet. Usually using a moving company will cost about $1,400, versus the $80 you’d have to spend on beers and dinner to get your friends to come help you move.

When you’re selling your home you generally want to make it as empty of as much clutter as possible. The best way to do this is to either find a very accommodating friend or family member who will let you dump your possessions somewhere in their house, or you can rent a storage unit. Storage PODS are a very popular method nowadays, and usually cost about $150 a month. Seeing how, in most U.S. markets, the listing period for a house for sale is about 30 to 40 days, that’s not too bad of a deal.

When you’re selling your home you generally want to make it as empty of as much clutter as possible. The best way to do this is to either find a very accommodating friend or family member who will let you dump your possessions somewhere in their house, or you can rent a storage unit. Storage PODS are a very popular method nowadays, and usually cost about $150 a month. Seeing how, in most U.S. markets, the listing period for a house for sale is about 30 to 40 days, that’s not too bad of a deal.

So all put together, it’s good to have an extra couple thousand dollars set aside for anything unexpected when creating a homebuying budget.

At this point we’ve reached the end of creating a homebuying budget. Get out our calculator and tally up the expenses and you’ll see you’ll want between $15K and $22K for a starter home of around $250K, assuming your down payment is between 3.5% and 6%. If you’re able to secure a 0% down payment loan, you could feasibly purchase a house for as little as $8K.

For homes in general, from starter houses to luxury estates, take 10% of the price plus an extra $3K and that’s generally how much money you’ll need to budget to purchase just about any home for sale in the United States. But your budgeting shouldn’t stop there.

Step Five: Prepare A Budget For Living In Your House

Just because you can afford to buy a house does not mean you can afford to live in it. When creating a homebuying budget, you should also create a second budget to give you an idea of how much you’ll be spending each month when living in your home. If you don’t plan ahead, you might wind up becoming house-poor, where your mortgage payments and other home-related expenses keep you from saving money, start cutting into your savings, and possibly lead to foreclosure.

Cost of living varies wildly across the U.S., so it makes more sense to plan in terms of proportion. Ideally, your home-related expenses, including mortgage payments, repair costs, and HOA fees, should not exceed 28% of your monthly income. Food and gasoline already take up a big chunk of your income, as do things like car insurance, car payments, and phone payments.

Cost of living varies wildly across the U.S., so it makes more sense to plan in terms of proportion. Ideally, your home-related expenses, including mortgage payments, repair costs, and HOA fees, should not exceed 28% of your monthly income. Food and gasoline already take up a big chunk of your income, as do things like car insurance, car payments, and phone payments.

But you don’t need us to tell you how much money you spend on all that. When creating a homebuying budget, try to factor out what kind of monthly mortgage payment you can afford. The average mortgage payment in the U.S. is $1,100, but that’s not all you’ll have to pay to keep your home. You also have to factor in HOA fees if you live in an area governed by an HOA. These monthly fees usually come to around $200 and $300 a month or $600 to $1500 a year, bumping your monthly home expenses to $1,400.

Next you have utilities, which are much more expensive in a home than in an apartment. Americans spend about $170 each month on utilities, though where you live and seasonal changes will affect this cost. Finally, home repairs and maintenance. Fixing a leak in your ceiling and mowing the grass all cost money. Home repairs, on average, cost about $170 a month, Add these costs to your mortgage and HOA payments, and you’re looking at $1,740 a month.

Interestingly enough, that’s still cheaper than renting. The median rent in the U.S. is nearing $2,000. So not only is owning a home cheaper than renting in the long run, but when you’ve built equity in your home and sold it, you’ll make more money than you would by moving out of your apartment. There’s technically no limit to how much money you can make from selling a house, while renting an apartment will always make you $0 at the end of the day.

Guide to Creating A Homebuying Budget – Conclusion

We hope this guide has prepared you for what you’ll need in your wallet when you buy a house, whether it be your first home or your fifth. It’s not as scary as it sounds, is it? Just so long as you’re prepared to pay for that home once you’ve bought it, (a little counterintuitive, we know), you’ll have no trouble being a successful homeowner.